Loans are essential financial tools that allow individuals and businesses to access money for important needs. Whether buying a home, financing education, or covering unexpected expenses, loans provide the necessary funds with the expectation of repayment over time, usually with interest.

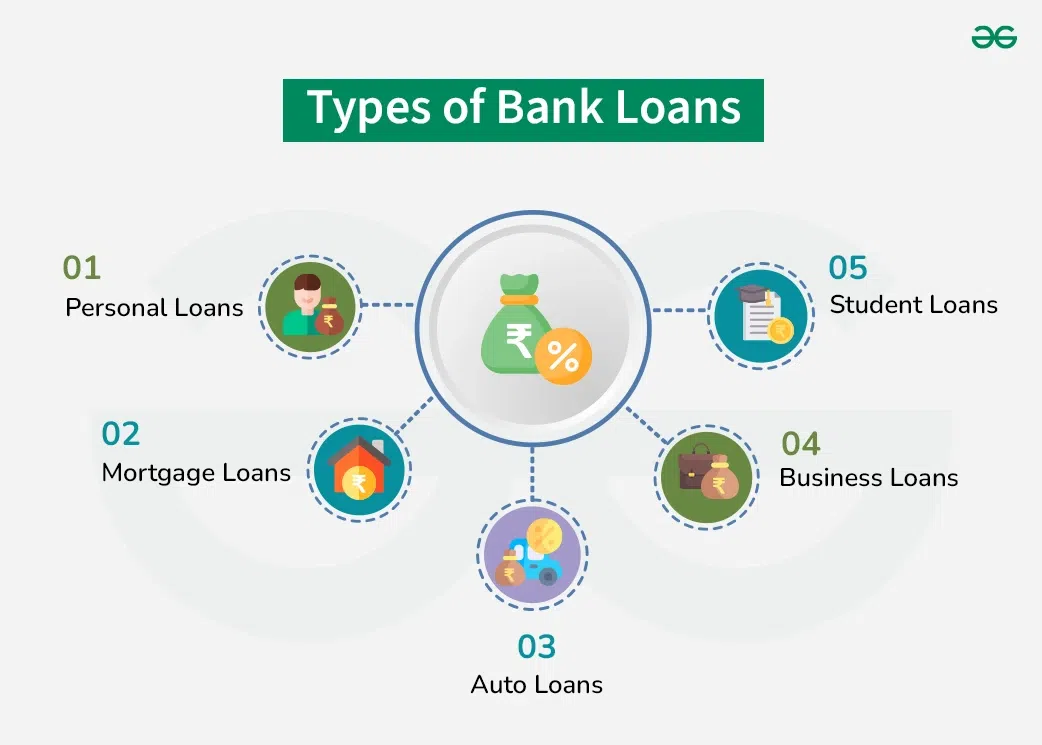

There are many types of loans, each designed for specific purposes. One of the most common types is the personal loan. Personal loans are typically unsecured, meaning they do not require collateral. They can be used for various purposes, including medical expenses, travel, debt consolidation, or emergencies. Interest rates depend on the borrower’s credit score and financial profile.

Another major type is the mortgage loan. Mortgages are used to purchase real estate and are secured by the property itself. Because mortgages involve large amounts and long repayment periods, interest rates are usually lower than unsecured loans. However, failure to repay can result in foreclosure, meaning the lender can take the property.

Auto loans are used to purchase vehicles. Like mortgages, they are secured loans, with the vehicle serving as collateral. These loans usually have fixed repayment terms, typically between three and seven years.

Student loans help finance education costs, including tuition, books, and living expenses. These loans often offer lower interest rates and flexible repayment options. Some student loans also provide deferred payments until after graduation.

Credit builder loans are designed to help individuals establish or improve their credit history. These loans are often offered by credit unions or financial institutions. The borrower makes payments over time, and the payment history helps build a positive credit profile.

Payday loans are short‑term loans designed to provide quick cash. However, they often have extremely high interest rates and fees, making them risky and expensive. Financial experts generally recommend avoiding payday loans whenever possible.

Secured loans require collateral, such as property, vehicles, or savings accounts. Because collateral reduces risk for lenders, secured loans often have lower interest rates. Unsecured loans, on the other hand, do not require collateral but typically have higher interest rates due to increased risk.

Interest rates can be fixed or variable. Fixed rates remain the same throughout the loan term, providing predictable payments. Variable rates can change over time based on market conditions, which may increase or decrease monthly payments.

Loan terms vary widely, ranging from short‑term loans lasting a few months to long‑term loans lasting decades. Longer terms usually result in lower monthly payments but higher total interest costs.

Before taking a loan, it is important to evaluate your financial situation carefully. Consider the interest rate, repayment period, fees, and total cost. Borrow only what you need and ensure you can repay it comfortably.

Loans can be valuable financial tools when used responsibly. They allow individuals to achieve important goals, manage emergencies, and invest in their future. However, misuse of loans can lead to debt problems and financial stress.

Understanding different loan types helps borrowers make informed decisions and choose the best option for their needs. Responsible borrowing ensures long‑term financial health and stability.